Renovation financing is defined as any loan product that funds home improvement costs, either by combining them with a mortgage or by borrowing against existing home equity. Understanding how renovation financing works is the first step to turning a project estimate into a funded plan. The main categories are home equity loans, home equity lines of credit (HELOCs), cash-out refinancing, renovation-specific mortgages like the FHA 203(k), Fannie Mae HomeStyle, and Freddie Mac CHOICERenovation, and unsecured personal loans. Each option carries different interest rates, collateral requirements, and timelines. Government programs through HUD, including Title 1 property improvement loans, add another layer of options for qualifying homeowners. Choosing the right path depends on your equity position, credit profile, and project scale.

What are the main types of renovation financing?

Homeowners can finance renovations through four broad categories: equity-based loans, renovation mortgages, unsecured personal loans, and government-backed programs. Each category serves a different financial situation and project size.

Equity-based loans and lines of credit

Home equity loans and HELOCs both borrow against the value you have built in your home. HELOCs allow borrowing up to about 85% of home value minus your outstanding mortgage balance, while home equity loans can reach up to 90%. HELOCs carry variable interest rates and work like a revolving credit line. Home equity loans deliver a lump sum at a fixed rate, which makes monthly budgeting more predictable. Cash-out refinancing replaces your existing mortgage with a larger one and gives you the difference in cash for renovations.

Renovation-specific mortgages

These products are built for buyers or owners who want to combine purchase and renovation costs into a single monthly payment. The FHA 203(k) is the most widely used government-backed renovation mortgage and is available to borrowers with lower credit scores. The Fannie Mae HomeStyle loan caps renovation costs at roughly 75% of the post-renovation appraised value, so the finished home’s worth drives how much you can borrow. Freddie Mac CHOICERenovation follows a similar structure and is underwritten on the anticipated completed value of the property.

Unsecured personal loans

Personal loans fund renovations faster, typically within about a week, compared to equity-based products. The trade-off is higher interest rates and shorter repayment terms. Personal loans work best for smaller or urgent projects where speed matters more than minimizing interest cost. They require no collateral, so your home is not at risk if repayment becomes difficult.

| Loan type | Collateral required | Rate type | Best for |

|---|---|---|---|

| Home equity loan | Yes (home) | Fixed | Large, planned projects |

| HELOC | Yes (home) | Variable | Phased or ongoing work |

| FHA 203(k) | Yes (home) | Fixed | Purchase plus renovation |

| Fannie Mae HomeStyle | Yes (home) | Fixed | Higher-value renovations |

| Personal loan | No | Fixed or variable | Small or urgent projects |

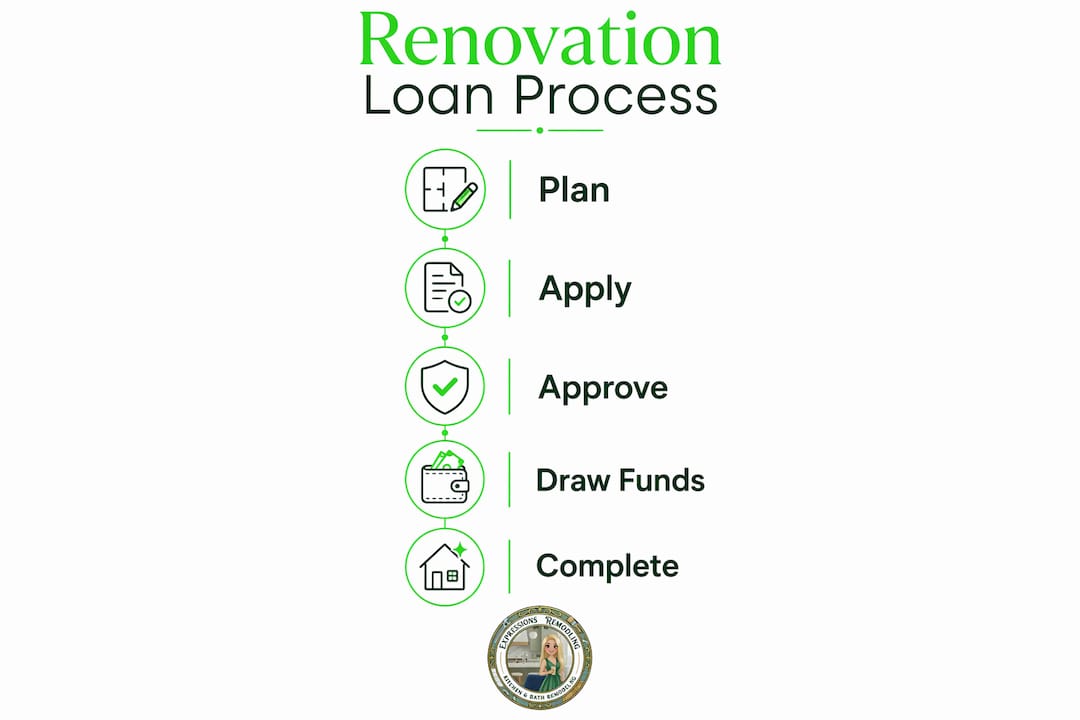

How does the renovation loan process work?

The renovation loan process follows a structured sequence that differs from a standard mortgage. Knowing each step prevents delays and protects your budget.

- Pre-approval. The lender reviews your credit score, income, debt-to-income ratio, and existing equity. You receive a conditional loan amount before you finalize contractor bids.

- Appraisal. The appraiser estimates both the current home value and the projected post-renovation value. Renovation mortgages like HomeStyle and FHA 203(k) base the loan amount on the completed value, not the current condition.

- Contractor approval and cost submission. Your contractor submits a detailed scope of work and cost breakdown. Lenders review this against the appraisal to confirm the numbers align.

- Loan closing. Renovation funds are placed into an escrow account at closing. You do not receive the full renovation budget upfront.

- Draw releases. Funds are released in stages as work is completed. FHA 203(k) renovation funds are held in escrow and released after inspections confirm each phase is done correctly.

- Inspections. Each draw request triggers an inspection. The inspector verifies completed work before the next payment goes to your contractor.

- Project completion. FHA 203(k) loans require project completion within 6–12 months depending on the loan version. Delays in inspections or contractor scheduling directly delay fund releases.

Pro Tip: Plan your contractor’s work schedule around the draw and inspection calendar before you close. Gaps between completed phases and inspection appointments are the most common cause of project delays on renovation loans.

FHA 203(k) loans require a contingency reserve of 10%–20% of renovation costs to cover unforeseen repairs. Any unused contingency funds can be applied to permanently affixed improvements at project end. This reserve is not optional. It is a built-in safeguard that lenders require, and it affects the total loan amount you request from day one.

A solid renovation project management plan helps you stay ahead of draw schedules and keep contractors on track throughout the process.

What factors determine loan eligibility and borrowing limits?

Lenders evaluate several factors before approving a renovation loan. Understanding these criteria helps you prepare a stronger application.

Credit score requirements vary by loan type:

- FHA 203(k): minimum 580 for the standard version (lower thresholds may apply with higher down payments)

- Fannie Mae HomeStyle and Freddie Mac CHOICERenovation: typically require a score of 620 or higher

- Home equity loans and HELOCs: most lenders prefer 620 or above, with better rates above 700

- Personal loans: available with lower scores, but rates rise sharply below 670

Debt-to-income ratio (DTI) is the percentage of your gross monthly income that goes toward debt payments. Most renovation mortgage programs cap DTI at 43%–45%. A lower DTI signals to lenders that you can absorb the added monthly payment.

Home equity is the difference between your home’s appraised value and your outstanding mortgage balance. Home equity borrowing power is highly sensitive to both the appraised value and your remaining mortgage payoff. A $400,000 home with a $250,000 mortgage gives you $150,000 in equity. A HELOC at 85% loan-to-value would allow borrowing up to $90,000 against that equity.

Closing costs and fees add real money to the total project cost. Renovation loans often carry additional closing costs of roughly 10%–15% of your renovation budget. These fees cover appraisals, inspections, lender origination charges, and escrow administration. Ignoring them when budgeting is one of the most common financial mistakes homeowners make.

Pro Tip: Get a Loan Estimate form from every lender you consider. Federal law requires lenders to provide this document within three business days of your application. It shows all fees in a standardized format so you can compare true costs side by side.

In HomeStyle renovation loans, contractor cost breakdowns must align precisely with lender appraisal expectations. If your contractor’s bid comes in higher than the appraiser’s cost assumptions, your borrowing capacity shrinks. Getting your contractor and appraiser on the same page early protects your loan amount.

What are the advantages and challenges of renovation financing?

Renovation financing gives homeowners real purchasing power, but every option carries trade-offs worth understanding before you sign.

Advantages:

- Renovation mortgages like CHOICERenovation and HomeStyle consolidate purchase and improvement costs into one payment, which simplifies monthly budgeting

- Secured loans (home equity loans, HELOCs) carry lower interest rates than unsecured alternatives because the lender has collateral

- FHA 203(k) loans are accessible to borrowers who cannot qualify for conventional renovation mortgages, broadening access to home improvement funding

- Government home repair programs through HUD provide additional options for veterans, low-income homeowners, and Native American borrowers

Challenges:

- Draw schedules and inspection requirements add complexity and paperwork, particularly with FHA 203(k) loans

- Delays in inspections or contractor work stall fund releases and can push projects past completion deadlines

- Secured loans put your home at risk if you default, which raises the stakes compared to unsecured borrowing

- Closing costs of 10%–15% of renovation costs can catch homeowners off guard if not factored into the initial budget

“The biggest mistake homeowners make is treating renovation financing like a simple bank loan. The escrow process, draw schedules, and inspection requirements mean your project cash flow depends entirely on how well you plan and document each phase.”

Mitigating these risks comes down to three things: building a realistic contingency reserve, maintaining clear communication with your contractor about draw timelines, and reading every loan document before closing. Homeowners who plan a home remodel with financing in mind from the start avoid the most common budget overruns.

How to choose the right renovation financing for your project

Matching the right loan to your project requires an honest assessment of four variables: project size, available equity, credit profile, and how quickly you need funds.

- Define your project scope and budget. Get at least two contractor estimates before approaching a lender. Vague budgets lead to underfunded loans and mid-project cash shortfalls.

- Calculate your available equity. Subtract your mortgage balance from your home’s current market value. If equity is limited, renovation mortgages or personal loans become the primary options.

- Check your credit score. Pull your credit report before applying. Errors are common and correcting them before a lender review can improve your rate.

- Match loan type to project scale. Large structural renovations fit FHA 203(k) or HomeStyle loans. Mid-size projects suit home equity loans or HELOCs. Small or urgent repairs align with personal loans.

- Compare Loan Estimates from multiple lenders. Rates, fees, and terms vary significantly between lenders offering the same loan product. Shopping at least three lenders is standard practice.

Pro Tip: If your project timeline is flexible, applying for a home equity loan or HELOC after a recent appraisal increase gives you the most borrowing power. Home values shift, and timing your application to a strong local market can meaningfully expand your budget.

Understanding the home modernization process before you apply helps you set realistic expectations for timelines and documentation requirements.

Key Takeaways

Renovation financing works best when you match the loan type to your equity position, credit score, project scale, and timeline before applying.

| Point | Details |

|---|---|

| Loan types vary by collateral | Secured loans offer lower rates; personal loans fund faster but cost more in interest. |

| Draw schedules drive timelines | FHA 203(k) funds release in stages after inspections, so project planning must align with draw dates. |

| Closing costs add up | Budget an extra 10%–15% of renovation costs for fees, appraisals, and escrow charges. |

| Equity determines borrowing power | HELOCs reach up to 85% of home value minus mortgage balance; home equity loans up to 90%. |

| Contingency reserves are required | FHA 203(k) mandates a 10%–20% contingency reserve built into the approved loan amount. |

What I’ve learned about renovation financing after years in the field

Most homeowners walk into the financing process focused entirely on the interest rate. That is the wrong starting point. The rate matters, but the draw schedule, inspection cadence, and contingency reserve structure will determine whether your project finishes on time and on budget far more than a quarter-point difference in APR.

The detail that surprises homeowners most is how tightly contractor cash flow ties to lender inspection approvals. A contractor who cannot get paid until an inspector signs off will slow down or stop work. That is not a contractor problem. It is a planning problem. You need to build inspection windows into your project schedule before the first nail goes in.

I also see homeowners consistently underestimate closing costs. An extra 10%–15% on top of your renovation budget is real money. On a $60,000 kitchen project, that is $6,000–$9,000 in fees that have nothing to do with the actual work. Budget for it from day one, not after you get the Loan Estimate.

My honest recommendation: talk to your remodeling contractor before you finalize your loan type. A contractor who has worked with renovation mortgages knows what documentation lenders expect, how to structure bids to align with appraisals, and how to keep work moving between draws. That coordination is worth more than any rate discount.

— Kierin

Expressions Remodeling and your funded renovation

Once your financing is in place, the real work begins. Expressions Remodeling works with St. Louis homeowners on kitchen, bathroom, and basement projects designed to fit real budgets and realistic timelines.

The team at Expressions Remodeling understands how draw schedules and inspection requirements affect project pacing. Every project is planned with those milestones in mind, so work stays on track and fund releases happen without unnecessary delays. Whether you are funding a kitchen remodel in St. Louis or a full basement finish, Expressions Remodeling coordinates the scope, timeline, and documentation your lender needs. See affordable renovation options that align with your financing plan.

FAQ

What is renovation financing?

Renovation financing is any loan product that funds home improvement costs, either by combining them with a mortgage or by borrowing against home equity. Common types include FHA 203(k) loans, home equity loans, HELOCs, and personal loans.

How long does the renovation loan process take?

The process from application to project completion typically runs 6–12 months for FHA 203(k) loans. Simpler products like personal loans can fund within about a week.

What credit score do I need for a renovation loan?

FHA 203(k) loans accept scores as low as 580. Conventional renovation mortgages like Fannie Mae HomeStyle generally require a score of 620 or higher.

Are renovation loan closing costs different from regular mortgage costs?

Renovation loans carry additional closing costs of roughly 10%–15% of your renovation budget, covering appraisals, inspections, and escrow administration on top of standard lender fees.

Can I use a renovation loan if I have little home equity?

Yes. FHA 203(k) and personal loans do not require significant equity. FHA 203(k) bases the loan on the projected post-renovation value, while personal loans require no collateral at all.